This is Part 3 of 4 from The Last Prescription Series.

← Part 2 – What is a Cure Worth? | Part 4 – The Cure Works →[🧠] Sapien Fusion Deep Dive Series | February 24, 2026

The winner is not necessarily American.

The first FDA approval for a CAR-T therapy in autoimmune disease is expected in the first half of 2026. The company filing that application is American. The clinical work behind it involved patients in Europe and the United States. The regulatory approvals that follow — EMA, NICE, Health Canada, the TGA, PMDA — will determine which companies actually reach the 17.9 million RA patients, and which remain confined to their home markets.

This is not a race with one finish line.

It is a race with seven finish lines, and the companies running it are not all in the same country.

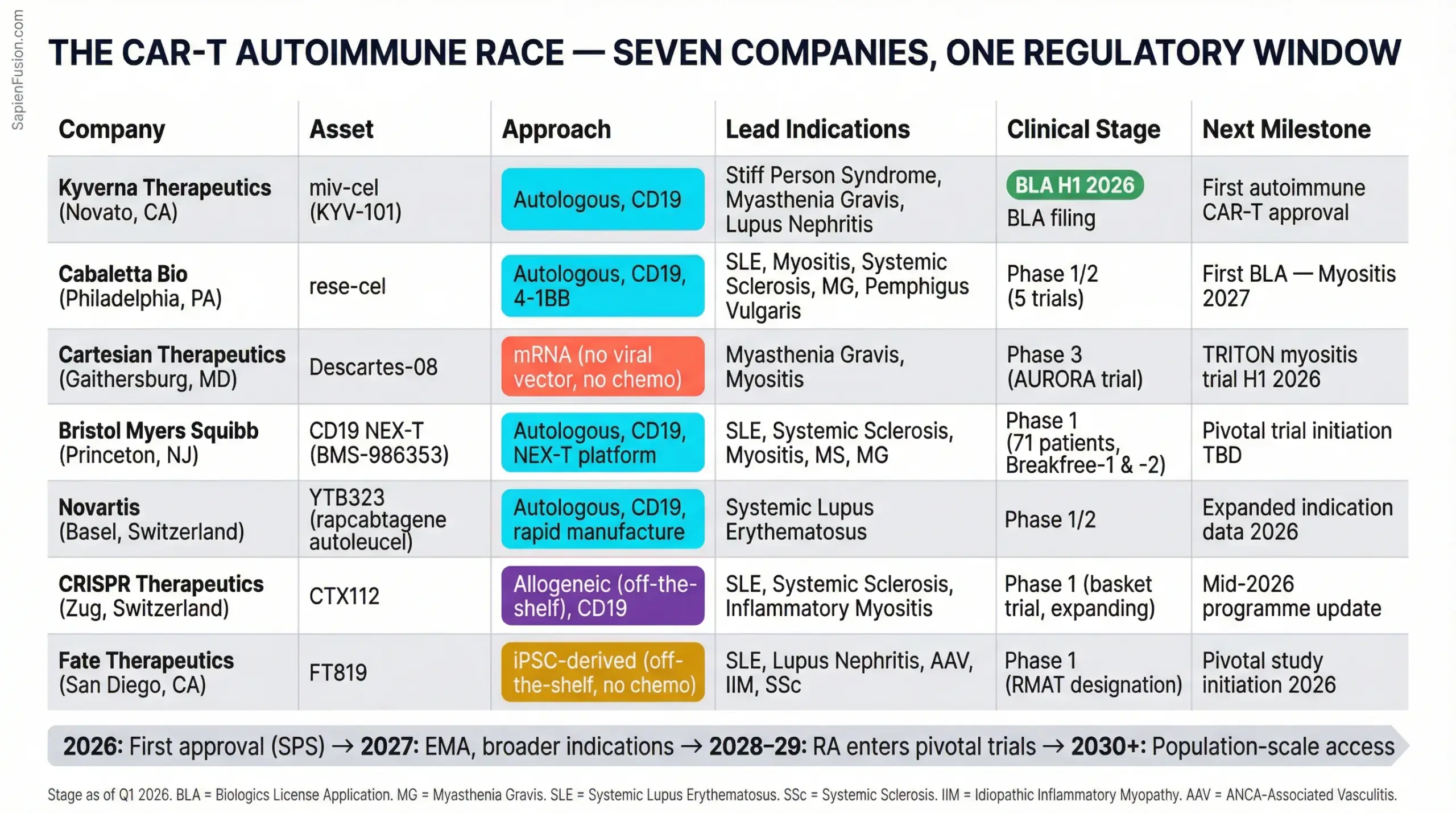

🇺🇸 Kyverna Therapeutics — Novato, California, USA

Status: Most advanced. BLA filing expected H1 2026.

Kyverna is the company closest to a regulatory approval in autoimmune CAR-T, and its lead indication is not RA or lupus — it is stiff person syndrome (SPS), a rare progressive neurological autoimmune condition affecting approximately 1 in 1,000,000 people. Fewer than 5,500 patients in the United States are diagnosed. The addressable market is tiny.

That is the point.

Rare disease approvals are faster, cheaper to run in clinical trials, and generate orphan drug designations that extend market exclusivity. Kyverna’s mivocabtagene autoleucel (miv-cel) achieved a 46% median improvement in the timed 25-foot walk test in its Phase 2 KYSA-8 registrational trial — a highly statistically significant result (p=0.0002). 81% of patients hit the clinically meaningful response threshold. All patients were off immunotherapy. None needed rescue treatment.

The stiff person syndrome filing is the beachhead. The real ambition is visible in Kyverna’s pipeline: miv-cel is also in Phase 3 for generalised myasthenia gravis, where it achieved a 100% response rate in a Phase 3 interim analysis — a number that rarely appears in clinical trial reports. Multiple sclerosis and rheumatoid arthritis are listed as exploration-stage indications.

Kyverna raised $319 million in its February 2024 IPO on Nasdaq. It has treated 100+ patients across multiple autoimmune diseases at sites globally. It has Regenerative Medicine Advanced Therapy (RMAT) designation and Orphan Drug designation for SPS in the US, and has maintained what its executives describe as “strong and consistent dialogue with the FDA.”

The strategic read: Kyverna is executing a classic rare-disease-first strategy — establish proof of regulatory success, build manufacturing credibility, then expand into larger indications. If miv-cel is approved for SPS in 2026, every subsequent filing — MG, MS, RA — arrives with a track record. The EMA filing will follow FDA. NICE assessment will follow EMA. The trajectory is visible.

The risk: Kyverna has one asset. Miv-cel’s clinical profile is strong, but the company’s entire valuation rests on a single therapy navigating multiple sequential regulatory processes. Any clinical, manufacturing, or safety setback reverberates across the entire pipeline.

🇺🇸 Cabaletta Bio — Philadelphia, Pennsylvania, USA

Status: Broadest clinical programme. First BLA targeted for 2027.

Cabaletta is running the most ambitious clinical programme in autoimmune CAR-T — not because it is the most advanced in any single indication, but because it is advancing simultaneously across the widest range of diseases. Its RESET programme covers: systemic lupus erythematosus, lupus nephritis, myositis (dermatomyositis and antisynthetase syndrome), systemic sclerosis, generalised myasthenia gravis, and pemphigus vulgaris.

Its asset, rese-cel, is a fully human CD19 CAR-T therapy using a 4-1BB co-stimulatory domain — a design choice that favours persistence over the CD28 approach Kyverna uses. The clinical data is compelling across multiple cohorts. In the RESET-SLE trial, 7 of 8 lupus patients with sufficient follow-up achieved DORIS or renal response criteria — the gold standard for lupus remission. 6 of 9 patients experienced zero cytokine release syndrome. All 9 were off all immunomodulators at data cutoff.

In systemic sclerosis — one of the most treatment-resistant autoimmune diseases, with high mortality from pulmonary fibrosis — all 4 patients meeting key inclusion criteria achieved clinically meaningful responses off all immunomodulators and steroids.

Cabaletta has FDA alignment on registrational cohort designs for lupus, myositis, and systemic sclerosis. FDA Fast Track Designation across dermatomyositis, SLE, lupus nephritis, systemic sclerosis, multiple sclerosis, and myasthenia gravis. RMAT designation in myositis and lupus. Its first BLA — targeting myositis — is planned for 2027.

A critical recent development: Cabaletta has received FDA clearance of an IND amendment to manufacture rese-cel using the automated, scalable Cellares platform. This matters enormously for Part 4’s manufacturing argument. Manufacturing at scale is the bottleneck for the entire field. Cabaletta is not waiting for approval to solve it.

The strategic read: Cabaletta is building a platform company, not a single-product company. If rese-cel works across six indications — and the early data suggests it does — Cabaletta becomes the company that owns the autoimmune CAR-T franchise. The breadth of its programme is its moat.

The risk: Running six simultaneous clinical programmes requires capital and execution discipline that few small biotechs sustain. Cabaletta’s market cap makes it an acquisition target. A larger company — BMS, Novartis, Roche — could absorb it before it reaches commercial scale. That may be the outcome Cabaletta’s investors are pricing in.

🇺🇸 Cartesian Therapeutics — Gaithersburg, Maryland, USA

Status: Technology differentiation. Phase 3 enrolling. Most globally accessible approach.

Cartesian is not trying to be first to approval. It is trying to be first to global scale — and its technology architecture makes that ambition credible.

Every other company in this space uses viral gene editing to permanently integrate the CAR construct into the patient’s T cells. Cartesian uses messenger RNA. The CAR is encoded in RNA, expressed transiently, then cleared. The T cells are not permanently reprogrammed. They function for the therapeutic window, then the engineering is gone.

This has two consequences that reshape the global access picture entirely.

No lymphodepletion required. The chemotherapy pre-conditioning that traditional CAR-T demands — cyclophosphamide and fludarabine, with their toxicity profiles, their inpatient requirements, their contraindications for patients with existing organ damage or who are of childbearing potential — is eliminated. Cartesian’s Descartes-08 is administered as six once-weekly outpatient infusions. No inpatient admission. No ICU backup. No chemotherapy.

Faster, simpler manufacturing. Viral vector production — the rate-limiting step in CAR-T manufacturing — costs over $16,000 per patient batch. mRNA manufacturing is orders of magnitude simpler and cheaper. A therapy that does not require viral transduction can be manufactured at a fraction of the cost and timescale of conventional CAR-T.

In Cartesian’s Phase 2b placebo-controlled trial in generalised myasthenia gravis — a rigorous design — Descartes-08 achieved 66.7% response rate. Zero cytokine release syndrome. Zero neurotoxicity. Patients tapered their prednisone dose by a median 55% at month 12. The Phase 3 AURORA trial is currently enrolling approximately 100 participants with acetylcholine receptor autoantibody-positive MG. The TRITON trial in myositis is initiating in H1 2026.

Cartesian also holds RMAT designation for Descartes-08 and has initiated a Phase 1/2 paediatric trial in juvenile dermatomyositis — a disease with essentially no effective treatment options and a patient population that cannot tolerate conventional CAR-T’s chemotherapy requirements.

The strategic read: Cartesian’s mRNA approach is not just a manufacturing simplification. It is the technology that makes autoimmune CAR-T viable in community rheumatology clinics in Canada, Australia, Germany, and Japan — not just in specialised oncology centres in Boston and London. The outpatient, no-chemotherapy profile expands the addressable setting globally in a way that conventional CAR-T cannot match.

The risk: mRNA-based CAR-T cells are transient. Whether a series of six weekly infusions achieves the deep, durable depletion that conventional persistent CAR-T achieves in a single infusion is the unresolved clinical question. If durability data shows shorter remissions requiring retreatment, the economics shift — though retreatment in an outpatient setting without chemotherapy may still compare favourably to lifetime biologics.

🇺🇸 Bristol Myers Squibb — New York, USA (with operations across 50+ countries)

Status: The established player moving deliberately. No approved autoimmune CAR-T. Watching everything.

BMS is the only company in this race that already has two approved CAR-T therapies — Breyanzi (liso-cel) for blood cancers and Abecma (ide-cel) for multiple myeloma. It knows how to manufacture CAR-T at commercial scale. It knows how to navigate FDA, EMA, and Health Canada for cell therapy approvals. It knows what post-approval reimbursement negotiations look like in every major market.

In February 2026, BMS launched the Autoimmunity Cell Therapy Network (ACTioN) — a consortium bringing together scientists, clinicians, and patient advocates to accelerate CAR-T development in autoimmune disease. The indications listed: SLE, multiple sclerosis, idiopathic inflammatory myopathies, systemic sclerosis, and myasthenia gravis. The structure: three pillars covering scientific evidence generation, clinical knowledge exchange, and ecosystem development for commercial adoption.

BMS is not disclosing specific clinical trial timelines or asset details for its autoimmune programme. It is building infrastructure.

The strategic read: BMS does not need to be first. It needs to be ready when the market is validated. Kyverna’s approval — if it lands in 2026 — validates the regulatory pathway. Cabaletta’s data validates the platform breadth. Cartesian’s data validates the outpatient model. BMS watches all three, absorbs the learnings, and enters with manufacturing scale, commercial infrastructure, and payer relationships that no biotech can match. The most likely BMS move is acquisition — of Cabaletta, Cartesian, or both.

The risk: Moving too slowly. If Kyverna or Cabaletta establishes category-defining clinical data and physician relationships in rheumatology before BMS has a competing asset, the gap may be difficult to close. Rheumatologists, unlike oncologists, are not accustomed to cell therapy. The first companies to educate and establish clinical protocols in rheumatology will have lasting influence on practice patterns.

🇨🇭 Novartis — Basel, Switzerland

Status: Independent programme in lupus. The European player with global reach.

Novartis is the only major non-American company with a disclosed CAR-T autoimmune programme and the resources to commercialise it globally. Headquartered in Basel, with manufacturing infrastructure across Europe, Asia, and North America, Novartis is positioned in ways that US-listed biotechs are not — particularly for EMA approval, European national reimbursement negotiations, and Asian market access.

Its asset is rapcabtagene autoleucel (YTB323), a rapidly manufactured CD19 CAR-T therapy in Phase 1/2 for severe refractory SLE. Biomarker data presented at ACR Convergence 2025 showed B cell compartment reset consistent with what other programmes have demonstrated. The manufacturing approach — rapid production designed to reduce the vein-to-vein timeline — directly addresses one of the field’s core constraints.

Novartis also announced in February 2026 that it will break ground on a new global biomedical research centre in San Diego — a 466,000 square-foot facility expected to house approximately 1,000 employees, integrating AI-enabled discovery for genetics, neuroscience, and oncology. The $23 billion US investment commitment signals long-term strategic intent in the US market, even from a Swiss-headquartered company.

The strategic read: Novartis has something the US biotechs lack: a credible path to simultaneous FDA and EMA approval, and the commercial infrastructure to execute reimbursement negotiations with NHS England, Germany’s GKV, France’s HAS, and Japan’s PMDA in parallel. If YTB323 delivers the clinical data, Novartis can execute a global launch that no Nasdaq-listed biotech can replicate.

The risk: Novartis is further behind in clinical development than Kyverna or Cabaletta. Being second to approval in a market defined by physician relationships and reimbursement precedents is a disadvantage that global scale can partially offset but not eliminate. The company that gets to NICE first sets the cost-effectiveness benchmark that all subsequent applicants are measured against.

🇨🇭 CRISPR Therapeutics — Zug, Switzerland (operations: Cambridge, Massachusetts, USA)

Status: Allogeneic differentiator. Phase 1 expanding. Pivotal timeline TBD.

CRISPR Therapeutics brings something none of the other players in this race have: a genuinely off-the-shelf, allogeneic CAR-T approach. Every other programme profiled here is autologous — the therapy is made from the patient’s own cells. CTX112 is made from a healthy donor, manufactured in advance, stored, and administered on demand. No apheresis. No weeks-long wait for a personalised manufacturing run.

The clinical asset is a CD19-targeting CAR-T built on CRISPR’s NEX-T platform, currently in Phase 1 for SLE under the basket trial designation. At the J.P. Morgan Healthcare Conference in January 2025, CEO Samarth Kulkarni announced expansion into systemic sclerosis and inflammatory myositis. Mid-2025 updates showed encouraging safety and pharmacodynamic data consistent with B cell depletion and immune remodelling.

The strategic logic of allogeneic CAR-T is compelling: standardised manufacturing, inventory on hand, dramatically lower per-patient cost if the platform matures. The clinical question — whether donor-derived cells achieve the depth and durability of autologous CAR-T without rejection — remains open. CRISPR Therapeutics built its reputation on answering hard questions. CTX112 is the bet that allogeneic can do what autologous does, at a fraction of the access barrier.

The strategic read: If CTX112 delivers comparable efficacy to autologous programmes, it resets the manufacturing economics of the entire field. A therapy available off-the-shelf changes who can offer it, where, and at what cost. CRISPR Therapeutics is not trying to win the first approval — it is trying to win the market that emerges after the first approvals prove the concept.

The risk: Allogeneic CAR-T has a history of clinical disappointment in oncology, where graft-versus-host disease and early cell exhaustion have limited durability. Autoimmune disease may prove more forgiving — patients are not immunocompromised in the same way, and the depth of depletion required may be more achievable. But the history of the platform warrants scrutiny that autologous programmes do not require.

🇺🇸 Fate Therapeutics — San Diego, California, USA

Status: Off-the-shelf iPSC platform. Phase 1 SLE. RMAT designation. Pivotal study planned 2026.

Fate Therapeutics is pursuing the most technically ambitious manufacturing model in the field. FT819 is derived not from a donor’s T cells but from induced pluripotent stem cells — a renewable, scalable starting material that can in principle produce unlimited quantities of standardised CAR-T product. The manufacturing implications, if the platform delivers clinically, are transformative: consistent product quality, no donor variability, inventory available at scale without per-patient apheresis or manufacturing runs.

In October 2025, Fate presented Phase 1 data from 10 SLE patients at ACR Convergence. Five patients surpassing three months of follow-up showed significant reductions in disease activity scores. Two lupus nephritis patients achieved complete renal response at six months. One patient remains in drug-free DORIS remission at 15 months. Across more than 60 patients treated with FT819 across autoimmune disease and oncology, the safety profile has been consistently favourable — low-grade cytokine release syndrome, no grade 3 or higher neurotoxicity, and critically, a conditioning-free regimen that does not require lymphodepletion chemotherapy.

Fate holds RMAT designation and is actively engaged with the FDA on a registrational study design, with a pivotal study targeted to initiate in 2026. Independent dose-expansion cohorts are open in ANCA-associated vasculitis, idiopathic inflammatory myositis, and systemic sclerosis — a breadth of indication expansion that signals confidence in the platform’s generalisability.

The strategic read: Fate is building toward the end-state that the entire field is pointing at: a CAR-T therapy that can be manufactured at population scale, stored, and administered without the per-patient manufacturing infrastructure that currently limits access. If the iPSC platform delivers durable remissions comparable to autologous programmes, Fate’s cost and access advantages become decisive. The company’s 600 cryopreserved drug product bags already in inventory — available for patient treatment today — is the most concrete demonstration of what off-the-shelf actually means in practice.

The risk: iPSC-derived cell therapies are newer and less clinically validated than T cell-derived approaches. Durability data beyond 15 months in autoimmune disease remains limited. The pivotal study design, once agreed with FDA, will determine whether Fate’s timeline to approval is competitive with the autologous leaders — or trails them by years.

The RA prize: 17.9 million patients, and nobody is there yet

Among all these programmes with seven companies, a dozen indications, two dozen clinical trials, one indication is conspicuously underdeveloped.

Rheumatoid arthritis. 17.9 million patients. The largest autoimmune disease population in the world. The largest biologic drug market. The disease most likely to drive a CAR-T reimbursement framework in every major healthcare system.

Only 10 RA patients have been treated with CAR-T globally in published literature. 9 of 10 achieved drug-free remission.

The reason RA is last is not because CAR-T does not work. It is because RA’s standard of care — biologics — works well enough that regulators require failure of at least two prior treatments before approving experimental therapies. The refractory RA population eligible for CAR-T under current trial criteria is smaller than the refractory lupus or MG population. There are fewer entry points.

That will change.

As manufacturing costs fall, as outpatient delivery becomes standard, as the safety profile is established across hundreds of patients in other indications, the risk-benefit calculation for earlier RA intervention will shift. A therapy proven safe and effective in lupus, myasthenia gravis, and systemic sclerosis will be studied in RA — first in refractory patients, then progressively earlier in the disease course.

The company that gets there first — whether Kyverna expanding from MG, Cabaletta expanding from its six-indication platform, Cartesian scaling its outpatient model, BMS acquiring its way in, or Novartis leveraging European infrastructure — inherits the largest autoimmune prize in the history of medicine.

No one has claimed it yet.

This is Part 3 of 4 from The Last Prescription

All parts in this series:

- Part 1 – Your Immune System has a Factory Reset

- Part 2 – What is a Cure Worth?

- Part 3 – Seven Companies are Racing to be First

- Part 4 – The Cure Works