[🧠] Sapien Fusion Deep Dive Series | February 24, 2026

The Alternative is Forever.

Every health economist who has ever modeled biologic therapy for rheumatoid arthritis has run the same calculation: cost of drug A versus cost of drug B, measured in quality-adjusted life years, assessed over a 10-year horizon. The number that comes out determines whether the drug gets listed on the formulary.

That model is built for a world where nothing cures the disease.

CAR-T cell therapy is not drug A or drug B. It is a one-time intervention that, in the patients treated so far, ends the disease. Running it through a cost-per-QALY model designed for chronic therapies produces a number that looks expensive. Running it through the right model produces a number that looks like infrastructure investment.

The right model has never been publicly run.

This is it.

What the drugs actually cost

The numbers that get quoted in US healthcare debates obscure the reality for the 17.9 million RA patients outside the American system. The economics look different depending on where you are, but they lead to the same conclusion.

🇺🇸 United States:

Commercial insurance, Medicare, and the uninsured

The US biologic market is structurally unlike any other, and it operates on at least three entirely different economic realities depending on who you are.

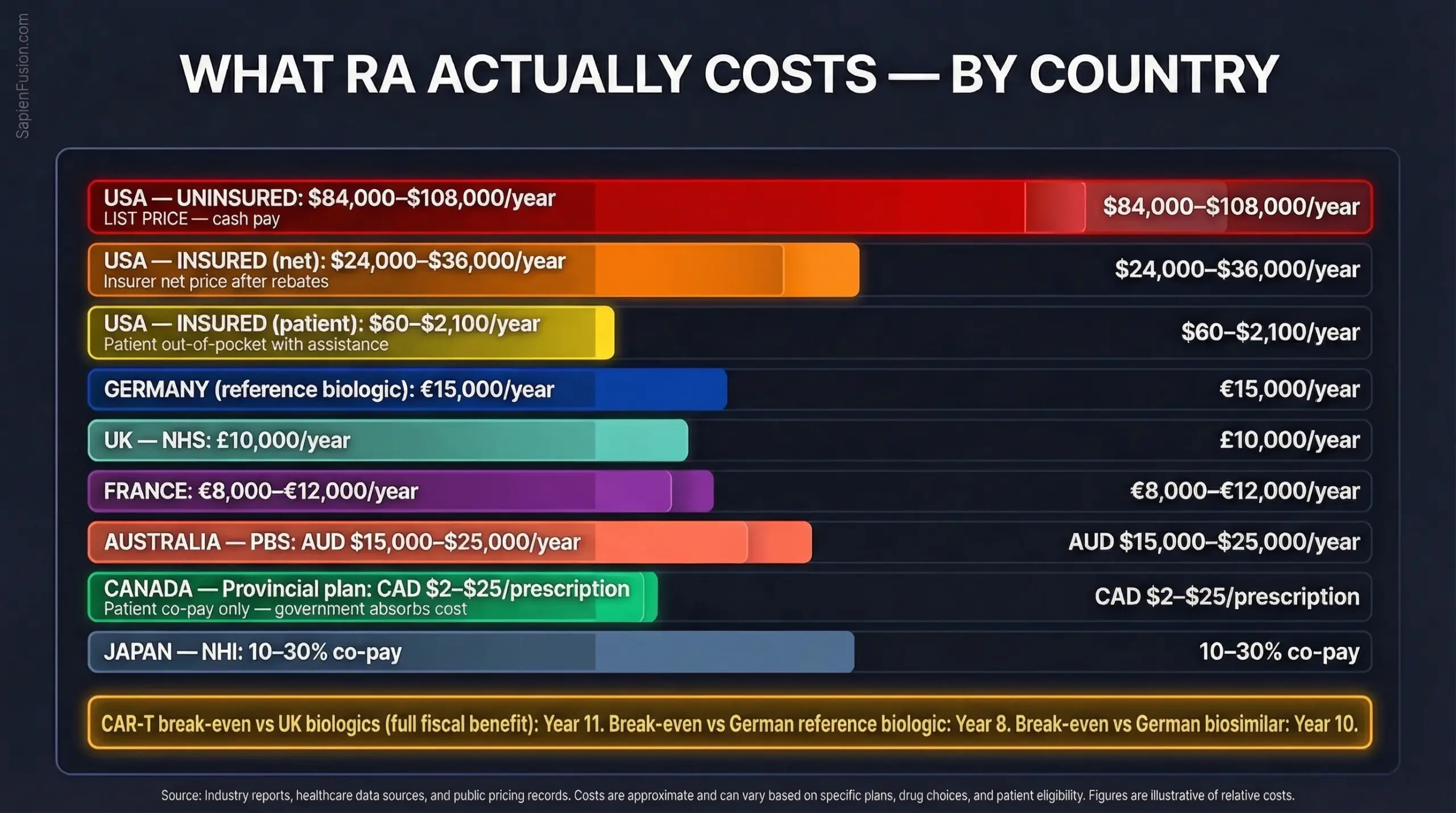

For commercially insured patients, Humira’s wholesale list price runs approximately $77,000 to $84,000 per year, but no insurer actually pays that. After rebate negotiations, commercial insurers pay a net price closer to $24,000 to $36,000 annually. Patients with access to AbbVie’s copay assistance card pay as little as $60 per year. The system is designed to make the drug appear affordable to the insured while extracting maximum value from payers.

For Medicare beneficiaries, the 2026 benefit cap limits out-of-pocket exposure to $2,100 annually. Enbrel’s list price exceeds $97,000 per year; Medicare negotiated it to approximately $94,821 from January 2026 under the Inflation Reduction Act, which still makes it one of the most expensive treatments on the negotiation list.

For the uninsured (approximately 25 to 30 million Americans), none of the above applies.

Without insurance

Humira costs $7,000 to $9,000 per month. That is $84,000 to $108,000 per year. In cash.

Enbrel without insurance runs over $8,000 per month or more than $96,000 annually. Biosimilar adalimumab products are available through discount programmes like GoodRx at roughly $550 per two-pack, which, at standard dosing, reduces the annual cash cost to approximately $13,200 — still more than the median individual income in many US states.

AbbVie operates a patient assistance programme (myAbbVie Assist) that provides free medication to uninsured patients who meet income eligibility requirements. It is a charity programme, not a right. Eligibility, application processing, and ongoing qualification create administrative burdens that many chronically ill, financially stressed patients cannot consistently navigate. The programme exists precisely because the list price would otherwise be inaccessible.

For an uninsured American with RA, the choice is often not between Humira and CAR-T. It is between Humira and nothing.

This is the context in which CAR-T reimbursement discussions happen in the United States.

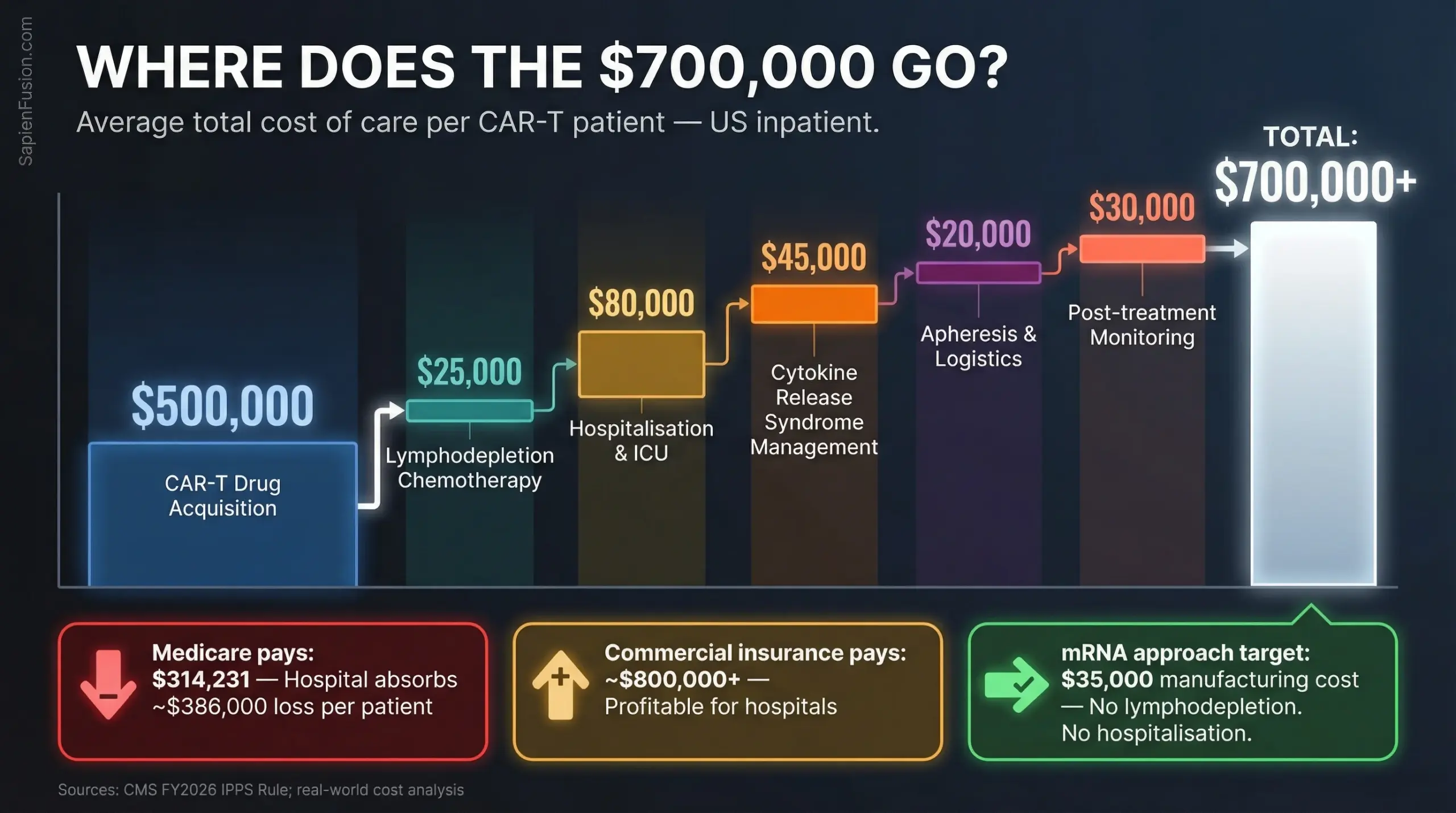

The gap that matters for CAR-T: Medicare’s current reimbursement for inpatient CAR-T (MS-DRG 018) is $314,231 for fiscal year 2026, while the actual total cost of care averages $700,000+. The gap is approximately $386,000 per patient. American hospitals running CAR-T programmes are absorbing that loss today for oncology. For autoimmune CAR-T, no reimbursement pathway exists yet. And for the uninsured, there is no pathway of any kind being discussed.

🇨🇦 Canada:

Provincial public drug plans

Canada’s system is provincial, not federal, which creates variation, but the underlying logic is consistent.

Provincial public drug plans cover RA biologics for eligible patients with patient co-payments typically ranging from CAD $2 to $25 per prescription (often covered by the pharmacy). The government absorbs the rest.

Canada has pursued biosimilar transitions aggressively: British Columbia’s Biosimilars Initiative alone saved CAD $732 million over five years by mandating transitions from originator biologics to approved biosimilars. Ontario, Alberta, and most other provinces have followed. Where the US still argues about whether biosimilars should be substituted, Canada has settled it and is reinvesting the savings.

For CAR-T, Health Canada approved the first cancer CAR-T products in 2019 and 2020. Provincial coverage decisions vary; some provinces cover them fully, while others require exceptional access applications. No provincial plan yet covers autoimmune CAR-T, because none is approved.

🇬🇧 United Kingdom:

NHS

Biologic therapy for RA costs the NHS approximately £10,000 per patient annually. Abatacept, one of the most commonly prescribed second-line biologics, was explicitly described in a King’s College London Lancet trial as costing “about £10,000 per patient per year.”

NICE approves drugs under strict cost-effectiveness thresholds — typically £20,000 to £30,000 per quality-adjusted life year. A drug that costs £10,000 annually and delivers moderate quality-of-life improvement tends to clear that bar.

A one-time treatment costing £400,000 does not clear it using the same formula.

The formula is wrong.

🇩🇪 Germany:

Gesetzliche Krankenversicherung (GKV)

Germany’s statutory health insurance system covers approximately 73 million people. Reference biologics for RA (the original branded versions) cost up to €15,000 annually.

Biosimilar competition following patent expiry has driven some adalimumab costs below €5,000 per year. The GKV operates a centralised benefits assessment body (IQWiG) designed for comparative drug assessment, not for evaluating one-time curative interventions.

🇫🇷 France:

Assurance Maladie

France’s public health system covers approximately 93% of healthcare costs for severe chronic diseases, including RA. Annual per-patient biologic spend runs €8,000 to €12,000.

France’s Haute Autorité de Santé (HAS) uses a five-tier clinical benefit rating. CAR-T’s data (drug-free remission in 84% of lupus patients, 9 of 10 RA patients) would likely be rated as a major added benefit.

Whether the reimbursement structure can accommodate the price is a separate question that hasn’t been answered yet.

🇦🇺 Australia

Pharmaceutical Benefits Scheme (PBS)

The PBS lists biologic DMARDs for RA at highly subsidised patient co-payments, typically AUD $31.60 per prescription at the general rate, with the government paying AUD $15,000 to $25,000 annually per patient.

Australia was one of the first systems to approve CAR-T for blood cancers. Its willingness to extend that framework to autoimmune disease will be instructive.

🇯🇵 Japan

National Health Insurance (NHI)

Japan covers RA biologics, with patients paying 10–30% co-payment. Japan approved its first CAR-T therapy in 2019 and has a structured cell therapy pathway. It has one of the world’s highest rates of biologic use in rheumatology and large RA patient volumes.

The lifetime calculation every government will eventually run

Here is the arithmetic that no health technology assessment body has yet published, but all of them will. And it does not start with the drug cost.

A patient diagnosed with RA at age 35 starts biologic therapy. She stays on it, with periodic drug switches due to loss of efficacy, for the rest of her working life. That is one visible number. But when she goes on long-term disability, and 1 in 3 RA patients becomes work-disabled within 5 years of diagnosis, the government’s fiscal exposure does not just grow. It inverts.

The government stops receiving her income tax and social contributions. In Germany, the average worker contributes approximately €20,000 annually in combined income tax and social contributions. In the UK, the equivalent figure is approximately £12,000 to £16,000 depending on earnings.

The government starts paying disability benefits. In Germany, the average erwerbsminderungsrente pays approximately €900 to €1,400 per month — €10,800 to €16,800 per year. In the UK, Employment and Support Allowance combined with housing benefit can reach £9,000 to £14,000 per year.

Healthcare costs rise. Work-disabled populations are heavier users of the healthcare system across all conditions, not just the primary diagnosis.

This is the calculation that transforms the economics entirely.

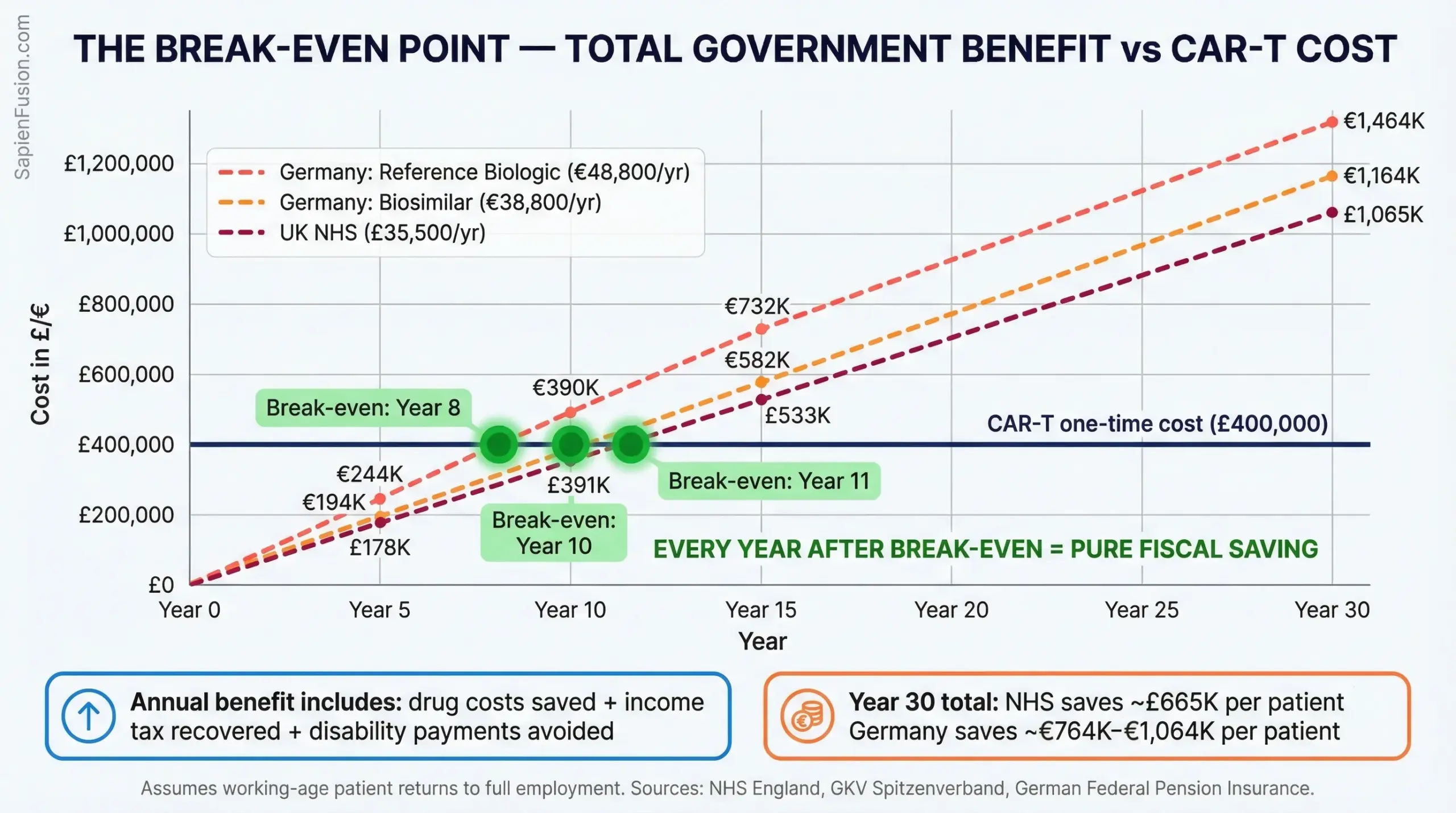

The break-even point is not drug cost versus drug cost. It is the year at which CAR-T’s one-time cost is recovered through everything the government stops spending and starts receiving again.

That full fiscal benefit — drug saved, tax recovered, disability avoided — runs to approximately £35,500 per year for an NHS patient returning to full employment, and €48,800 per year for a German patient on reference biologic pricing. Against a one-time CAR-T cost of £400,000:

The break-even point is Year 11 at UK pricing. Year 8 at German reference biologic pricing. Year 10 at German biosimilar pricing.

Every year after that point is pure fiscal recovery.

By year 30, the NHS net saving is approximately £665,000 per patient. Germany’s net saving reaches €764,000 to €1,064,000 per patient depending on drug pricing. At even modest volumes, 10,000 NHS patients treated, that is a £6.7 billion net fiscal gain over a generation.

The one-time treatment cost does not look like a cost at all. It looks like a government bond — with an eight-to-eleven-year payback and thirty years of compounding return.

The accountants running drug-versus-drug cost-effectiveness models are asking the wrong question, because the frameworks were built for a world where nothing cures the disease.

That world has ended.

The Scenario That Makes This Analysis Obsolete

Everything above assumes the current autologous CAR-T cost structure. £400,000 drug acquisition, lymphodepletion chemotherapy, hospitalisation, CRS management.

Cartesian Therapeutics is building something different. Descartes-08 uses mRNA instead of a viral vector. No lymphodepletion. No hospitalisation. Manufacturing cost target: $35,000.

If that holds at scale, the break-even calculation doesn’t shift — it disappears. A $35,000 intervention that returns a working-age patient to full employment recovers its cost in tax revenue alone within two years. The policy question stops being “can we afford this?” and becomes “why are we still paying for biologics?“

Cartesian’s TRITON myositis trial readout is expected H1 2026. That data will either validate the mRNA approach or reset expectations for the entire field.

Who loses, and where they are headquartered

The economic logic of CAR-T is hostile to the companies that currently profit from lifetime treatment. The exposure is global.

AbbVie

AbbVie

North Chicago, Illinois, USA. Humira (adalimumab) generated $14.9 billion in global net revenues in 2023, down from its peak as biosimilar competition intensified but still dominant. RA remains a core indication. AbbVie has no disclosed CAR-T autoimmune programme.

Amgen

Thousand Oaks, California, USA. Enbrel (etanercept) generated approximately $4.1 billion in 2023 global revenues. Amgen acquired Otezla from Bristol Myers Squibb in 2019; it is not positioned in CAR-T for autoimmune disease.

UCB

UCB

Brussels, Belgium. Cimzia (certolizumab pegol) and Bimzelx are core RA and psoriasis assets. UCB has no disclosed CAR-T autoimmune programme.

Pfizer

New York, USA. Xeljanz (tofacitinib) and Enbrel (ex-US rights through partnership) represent its RA exposure. Pfizer has made investments in cell therapy but not in autoimmune CAR-T specifically.

Roche / Genentech

Roche / Genentech

Basel, Switzerland. Actemra (tocilizumab) and Rituxan (rituximab) are both used in RA. Rituxan is an anti-CD20 B-cell depleting antibody — the same therapeutic logic as CAR-T, executed less completely. Roche understands the mechanism better than almost any other company. It has not announced an autoimmune CAR-T programme, but it is watching closely.

None of these companies face overnight disruption. CAR-T will reach a small refractory population first. Manufacturing constraints will limit volume for years. But the structural threat to $30+ billion in annual global autoimmune biologic revenues is real and the timeline is visible.

The reimbursement model that does not exist yet

No healthcare system in the world currently has a framework designed to pay for autoimmune CAR-T. The frameworks that exist were built for:

- Chronic drug therapies — annual cost assessed against annual benefit

- Oncology CAR-T — one-time treatment in a terminal-disease context where long-term savings are moot

Neither framework fits a one-time treatment that cures a chronic disease in a working-age population.

The models that will be required — and that some systems are already discussing — include:

Outcomes-based payment — the government pays a fraction upfront and the remainder only if remission is sustained at year one, year three, year five. Risk shared between manufacturer and payer.

Annuitised payments — the full treatment cost spread across the years of expected benefit, matching cash outflow to savings inflow. The treatment costs £40,000 per year over 10 years rather than £400,000 upfront.

Workforce investment framing — CAR-T assessed not as a medical intervention but as an economic productivity investment, evaluated against disability costs and tax recovery rather than drug-versus-drug cost-effectiveness.

The healthcare systems that develop these frameworks first — and the executives who understand them now — will be positioned to negotiate, approve, and fund the next generation of curative therapies not just for RA, but for the full range of autoimmune conditions that CAR-T is advancing toward.

The therapy exists. The payment model does not. That gap is a strategic opportunity.

What this means for decision-makers now

The economics of CAR-T for autoimmune disease are not a future consideration. The clinical data is published. The first FDA approval in this category is expected in 2026. EMA, NICE, IQWiG, HAS, PMDA, and the TGA will all be evaluating within the following 12 to 24 months.

Executives across healthcare systems, insurance, reinsurance, hospital networks, and pharmaceutical strategy need to be in this conversation before the frameworks are set — not after.

The companies racing to the clinic are profiled in Part 3. The manufacturing constraint that will determine how quickly this scales is in Part 4.

The economics are clear. The question now is execution.