This is Part 4 of 4 from The Last Prescription Series.

← Part 3 – Seven Companies are Racing to be First | The Last Prescription →[🧠] Sapien Fusion Deep Dive Series | February 24, 2026

The factory does not exist yet.

Every argument made in this series — the science, the economics, the company race — rests on a single assumption: that the therapy can be made. Not in a clinical trial. Not for 10 patients or 100. For hundreds of thousands of patients across dozens of countries, manufactured consistently, delivered on time, at a cost that healthcare systems can actually pay.

That assumption is not yet justified.

The science is ready.

The clinical data is published.

The regulatory path is open.

The factory is the problem.

Understanding the manufacturing constraint is not a technical footnote to the CAR-T story. It is the story. It determines who gets access, when, at what cost, and in which countries. Every other part of this series describes what is possible. This part describes what stands between possible and real.

How CAR-T is made — and why it breaks at scale

Conventional CAR-T manufacturing is a bespoke, per-patient process. There is no batch production. There is no inventory. Every treatment starts from scratch.

The process — called vein-to-vein — works like this:

A clinician draws blood from the patient. T cells are separated from the blood through a process called leukapheresis. The T cells are shipped, typically frozen, to a centralised manufacturing facility. At the facility, the cells are activated, then exposed to a viral vector — a modified virus engineered to carry the CAR gene — which inserts the genetic instruction into each cell. The modified cells are expanded in culture until there are enough to constitute a therapeutic dose, typically several hundred million cells. They are tested for safety and potency. They are frozen. They are shipped back to the treating centre. The patient is given chemotherapy to deplete their existing immune cells. Then the CAR-T product is thawed and infused.

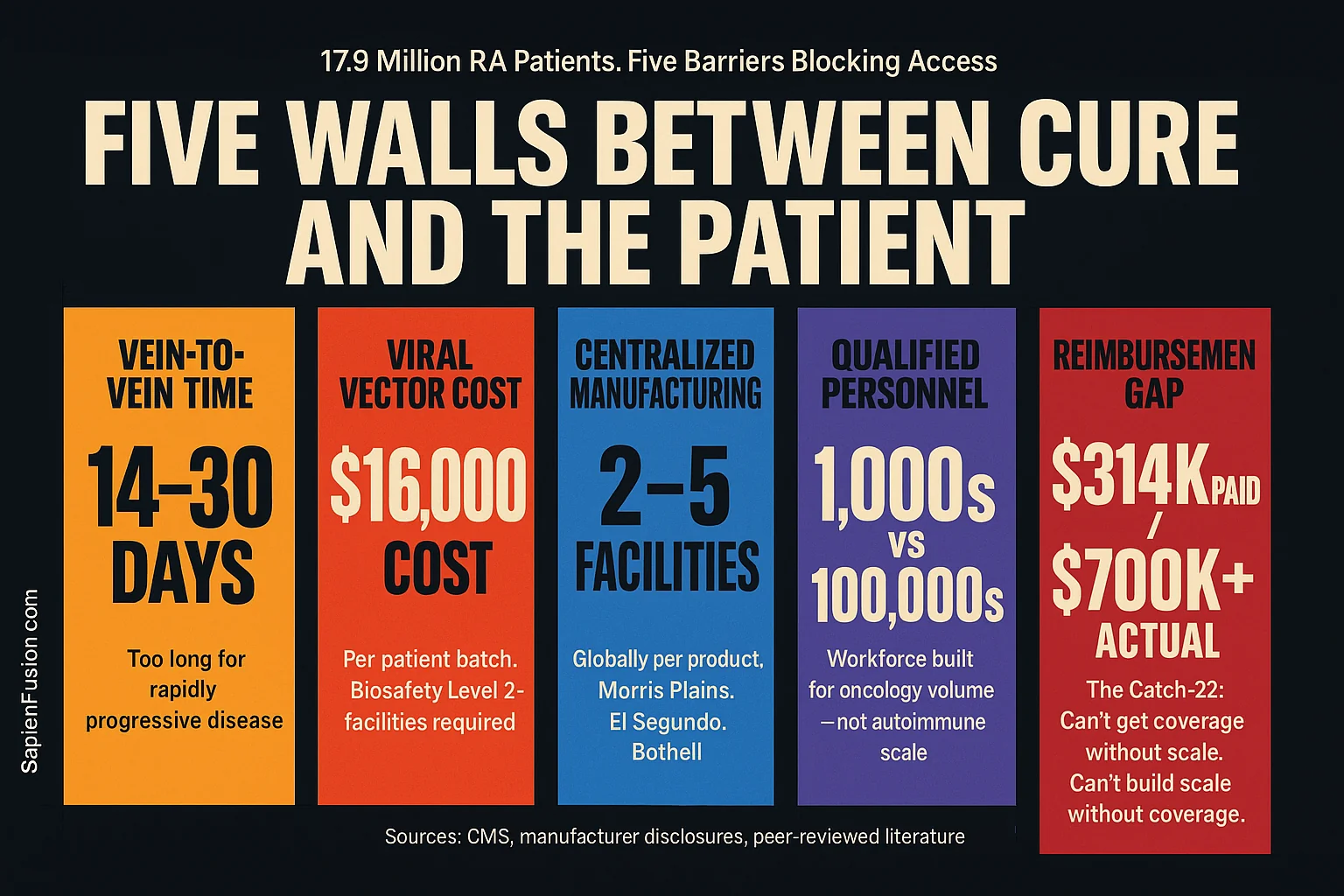

From blood draw to infusion: 14 to 30 days. Sometimes longer.

The viral vector alone — the engineered virus used to deliver the gene — costs over $16,000 per patient batch to produce at clinical grade. The full manufacturing process, including personnel, facility, quality control, and logistics, runs $173,000 to $600,000 per patient depending on the product and manufacturer. Total cost of care, including hospitalisation, chemotherapy, and monitoring, averages over $700,000.

That cost structure was designed for oncology. For a patient with relapsed leukaemia who has exhausted every other option, a $700,000 one-time treatment is justifiable. For a 38-year-old with RA who has failed two biologics but is otherwise healthy, the risk-benefit and cost-benefit calculations are different — and the manufacturing infrastructure does not fit.

To reach the 17.9 million RA patients, CAR-T manufacturing needs to be fundamentally rebuilt.

The five constraints that define the bottleneck

1. Vein-to-vein time

14 to 30 days is too long for patients with rapidly progressive disease. A patient with acute lupus nephritis destroying kidney function, or myositis progressing to respiratory failure, cannot wait a month for a manufacturing slot. In current trials, patients sometimes deteriorate during the wait and become ineligible for the treatment they enrolled to receive.

For RA — where the disease timeline is measured in years, not weeks — vein-to-vein time is less immediately critical. But it creates operational complexity: patients must be stable enough to wait, clinics must coordinate apheresis scheduling with manufacturing slots weeks in advance, and any manufacturing failure triggers a restart of the entire process.

2. Viral vector cost and complexity

Viral vectors — lentiviral or retroviral — are the delivery mechanism that inserts the CAR gene into T cells. They are expensive to produce, difficult to scale, and require biosafety level 2 or higher facilities with specialist equipment and personnel. A single manufacturing run producing enough vector for one patient costs over $16,000. A manufacturing run producing enough vector for 1,000 patients does not cost $16 million — the economics of vector manufacturing do not scale linearly. Capacity is the constraint, not just cost per unit.

Global viral vector manufacturing capacity was built for gene therapy trials, not for millions of autoimmune patients. Demand already exceeds capacity. Every new CAR-T programme approved adds pressure to a supply chain that was not designed for volume.

3. Centralised manufacturing geography

Every approved CAR-T product is manufactured at a small number of facilities — typically two to five globally per product. Tisagenlecleucel (Kymriah) is manufactured at Novartis facilities in Morris Plains, New Jersey, and Stein, Switzerland. Axicabtagene ciloleucel (Yescarta) is manufactured by Kite/Gilead in El Segundo, California, and Amsterdam. Lisocabtagene maraleucel (Breyanzi) is manufactured by Bristol Myers Squibb in Bothell, Washington, and Leiden, Netherlands.

A patient in Tokyo, Sydney, São Paulo, or Lagos ships their cells to one of these facilities, waits three to four weeks, and receives their product back — if the manufacturing run succeeds and the logistics chain holds. Cold chain failures, customs delays, and apheresis product quality issues cause manufacturing failures that require the entire process to restart.

For the countries that will carry the largest patient volumes — China, India, Brazil, Japan — a manufacturing model dependent on North American and European facilities is not viable at scale. Access will be confined to the small number of patients whose healthcare systems can fund international logistics and whose clinical condition can tolerate the timeline.

4. Qualified manufacturing personnel

CAR-T manufacturing requires specialists who understand both cell biology and GMP (Good Manufacturing Practice) pharmaceutical production. These people are rare. Training takes years. The current global workforce of qualified CAR-T manufacturing personnel was calibrated for oncology volumes — a few thousand patients per year globally. Scaling to tens or hundreds of thousands of autoimmune patients requires a workforce that does not currently exist and cannot be created quickly.

5. The reimbursement gap that makes building the factory financially irrational

Here is the constraint that makes all the others worse: the manufacturing investment required to solve the bottleneck will not be funded if reimbursement does not support it.

In the United States, Medicare pays $314,231 for inpatient CAR-T while actual costs average $700,000+. Hospitals running CAR-T programmes are absorbing losses on every Medicare patient treated. That loss structure does not incentivise the capital investment required to build decentralised, high-volume manufacturing infrastructure. It incentivises the opposite — restricting access to patients whose insurance pays commercial rates, concentrating programmes at academic centres that can cross-subsidise from other revenue streams.

In countries with government-funded health systems — the UK, Canada, Australia, Germany, France — no reimbursement pathway for autoimmune CAR-T yet exists. Health technology assessment bodies cannot price a therapy that has not been approved. Manufacturers cannot invest in manufacturing capacity for markets that have not committed to coverage. The investment required to build the factory precedes the revenue that would justify building it.

This is the Catch-22 at the centre of the bottleneck. You cannot get coverage without manufacturing at scale. You cannot build manufacturing at scale without coverage.

What is being built to solve it

Automated manufacturing platforms

Cabaletta Bio has received FDA clearance of an IND amendment to manufacture rese-cel using the Cellares platform — an automated, closed-system manufacturing device designed for scalable CAR-T production. The Cellares Cell Shuttle automates the full manufacturing workflow — activation, transduction, expansion, formulation — in a closed system that reduces manual handling, contamination risk, and batch-to-batch variability. Automated manufacturing reduces the skilled labour requirement per batch, enables parallel processing of multiple patient products, and is compatible with decentralised deployment at clinical sites rather than centralised manufacturing hubs.

Clinical manufacturing data from the Cellares platform is expected in the first half of 2026. If GMP readiness is confirmed, Cabaletta becomes the first autoimmune CAR-T programme with a validated pathway to scalable, automated manufacturing — a competitive advantage that extends beyond clinical data.

mRNA-based CAR-T — eliminating the vector entirely

Cartesian Therapeutics’ mRNA approach eliminates the viral vector constraint at the source. No viral transduction means no viral vector to manufacture, no viral vector supply chain, and no viral vector cost. mRNA production is faster, cheaper, and more amenable to scale than viral vector production. The manufacturing timeline for mRNA-based cell therapies is measured in days, not weeks.

The outpatient delivery model removes the hospitalisation infrastructure requirement. A therapy delivered as six once-weekly outpatient infusions without chemotherapy pre-conditioning can be administered at any rheumatology clinic with an infusion suite — not just at specialised cancer centres with bone marrow transplant units. That is the geography of RA care, not the geography of CAR-T care. Closing that gap is what takes this therapy from 100 patients to 100,000.

Point-of-care manufacturing

The most radical near-term solution to the centralised manufacturing problem is making CAR-T at the treatment site — in the hospital or clinic where the patient is treated. Point-of-care (POC) manufacturing eliminates international logistics, cold chain risk, customs delays, and vein-to-vein time driven by shipping. It reduces costs: in-house production cost estimates as low as $35,000 have been reported when viral vector is sponsor-supplied, compared to $173,000 to $600,000 for centralised manufacture.

Several automated POC manufacturing devices are in development. None are commercially available in the United States yet, but the infrastructure investment is underway. Companies that establish POC manufacturing in 2026 to 2028 will be positioned to serve markets that centralised manufacturers cannot — community hospitals, regional centres in Japan, Australia, and Canada, and eventually clinical settings in middle-income countries.

Contract Development and Manufacturing Organisations (CDMOs)

The CDMO sector is scaling aggressively to meet projected cell and gene therapy demand. Lonza, Wuxi ATU (China), Catalent, and Thermo Fisher Scientific are among the global CDMOs that have invested hundreds of millions in cell therapy manufacturing infrastructure. For smaller autoimmune CAR-T companies without proprietary manufacturing, CDMOs provide a path to commercial scale without the capital expenditure of building facilities. For Kyverna and Cabaletta specifically, CDMO partnerships will determine whether manufacturing can support commercial launch volumes if and when approvals arrive.

The realistic timeline — globally

2026: First autoimmune CAR-T approval (US, Kyverna for SPS). Commercial manufacturing at small volume. Restricted to specialised centres in the US, likely 5 to 15 sites. EMA submission initiates.

2027: EMA approval likely for first indication. NICE assessment begins. Health Canada, TGA, and PMDA reviewing. Cabaletta BLA for myositis filed. Reimbursement negotiations begin with NHS England, Germany’s GKV. Automated manufacturing platforms entering clinical validation.

2028 to 2029: Broader indication approvals across lupus, myasthenia gravis, myositis. Reimbursement frameworks established in UK, Germany, France, Australia, Japan. Manufacturing capacity expands through CDMO scale-up and first POC deployments. Cartesian AURORA trial reads out; mRNA model validated or challenged.

2030 and beyond: RA indication enters pivotal trials. Outpatient delivery becomes standard for appropriate patients. POC manufacturing viable in regional centres. Cost per patient begins meaningful decline as automation matures. Access expands to middle-income markets. The 17.9 million RA patients become a realistic addressable population rather than a theoretical one.

For the uninsured in the United States — the 25 to 30 million Americans without coverage — that timeline extends indefinitely unless reimbursement reform or manufacturer assistance programmes create a pathway. The manufacturing can be scaled. The access problem in the US is not technological.

It is political.

What this means for decision-makers now

The manufacturing bottleneck is not a reason to dismiss CAR-T for autoimmune disease. It is a map of where the strategic opportunities lie.

For healthcare systems — NHS, GKV, Assurance Maladie, OHIP, Medicare — the opportunity is to develop reimbursement frameworks before approvals land, not after. The systems that have pricing models ready when Kyverna or Cabaletta files for national approval will move faster, pay less, and capture the workforce and fiscal benefits described in Part 2 years ahead of systems that are still running their cost-effectiveness assessments.

For hospital networks and health systems — the opportunity is infrastructure investment: infusion suite capacity, trained rheumatology staff, apheresis capability, and patient selection protocols. The centres that are ready when the first approvals arrive will capture patient volumes that define practice patterns for a generation.

For investors — the companies solving the manufacturing constraint are as important as the companies developing the clinical assets. Cellares, automated manufacturing platform companies, and CDMOs building cell therapy capacity are infrastructure plays on a market that does not yet fully exist. The infrastructure investment precedes the market by three to five years.

The cure is not coming.

The cure is here.

The question is whether the world can build the systems to deliver it.

This is Part 4 of 4 from The Last Prescription

All parts in this series:

- Part 1 – Your Immune System has a Factory Reset

- Part 2 – What is a Cure Worth?

- Part 3 – Seven Companies are Racing to be First

- Part 4 – The Cure Works