This is Part 6 of 7 from The Capital Efficiency Paradox Series.

← Part 5: From 20 Researchers to 2.7 Billion Downloads | Part 7: The Capital Efficiency Playbook →

[🧠] Sapien Fusion Deep Dive | February 17, 2026

When Deployment Metrics Mask Customer Churn

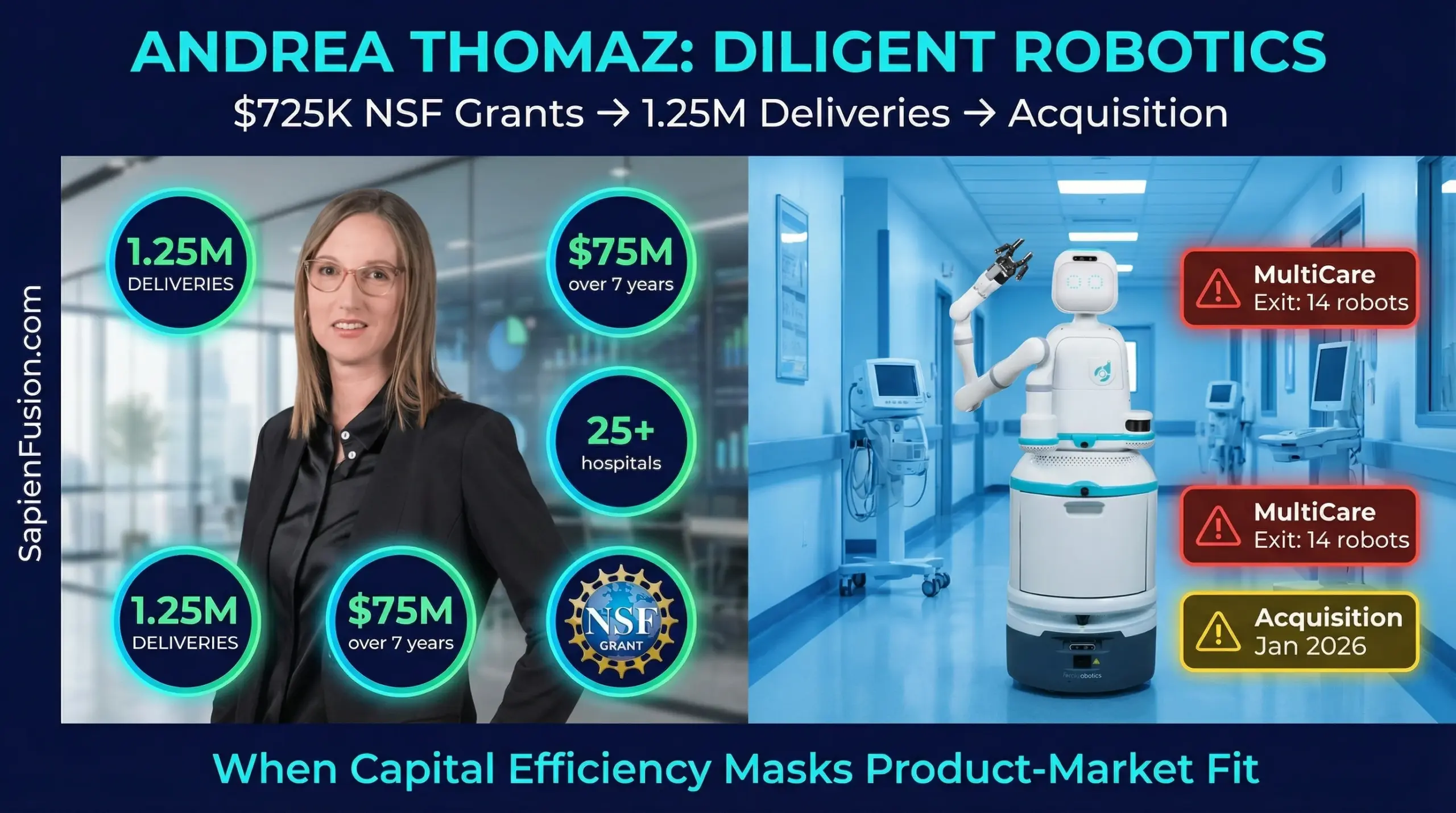

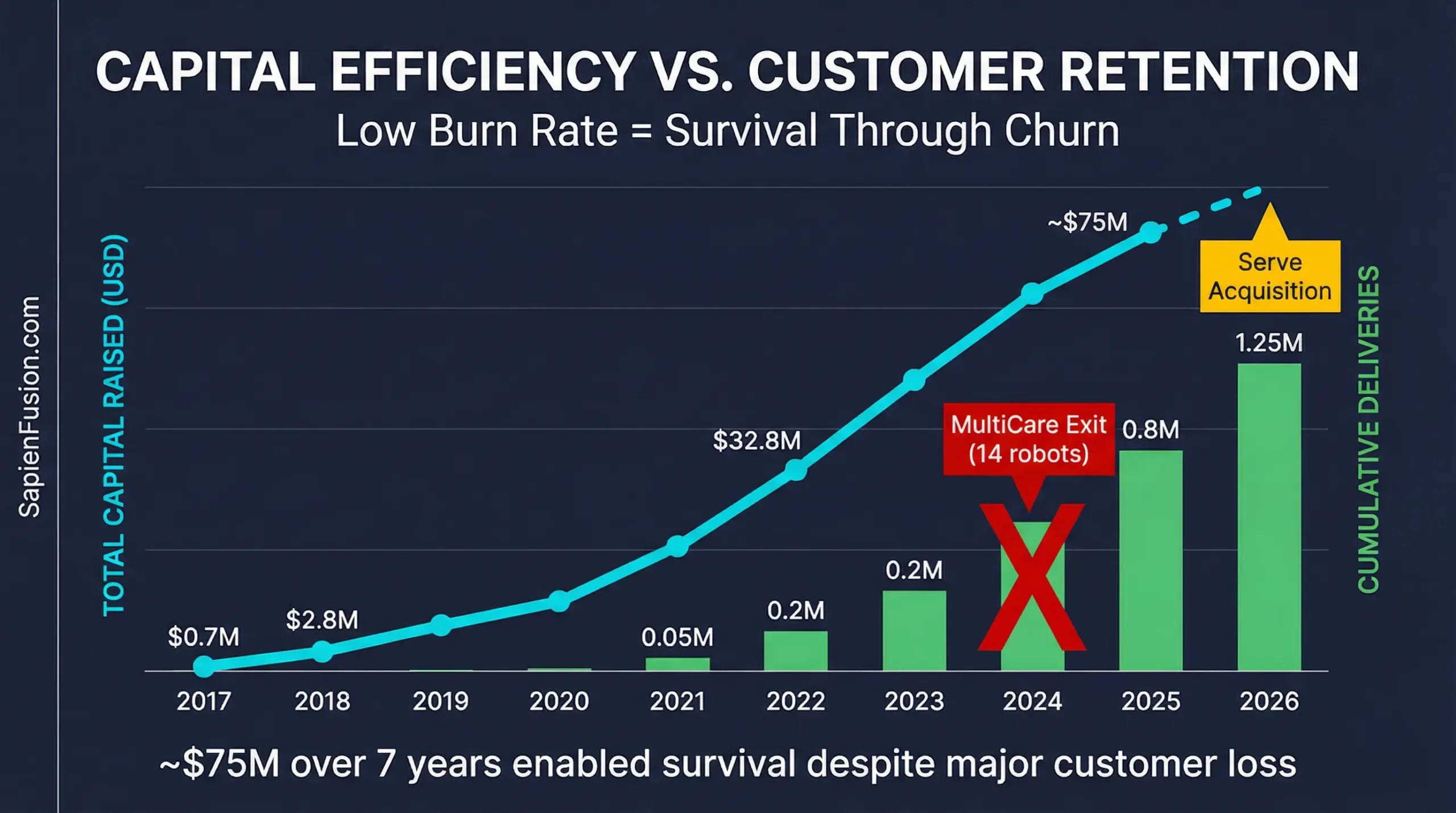

Twenty years. One technical obsession. $725,000 in NSF grants before venture capital. By February 2025, Andrea Thomaz‘s Diligent Robotics had deployed robots that completed 1.25 million deliveries across 25+ hospitals—navigating elevator crowds, dodging stretchers in narrow corridors, and generating terabytes of training data weekly.

But capital efficiency can obscure what deployment metrics don’t reveal: actual customer value.

While Diligent announced its millionth delivery milestone in February 2025, one of its larger customers—MultiCare Health System in Tacoma, Washington—had quietly terminated its contract approximately one year earlier. After deploying 14 Moxi robots across its facilities, MultiCare determined the system “wasn’t financially sustainable” and that “the cost didn’t justify their level of usage.”

Nurses at MultiCare hospitals reported the robots were “annoying and often got in the way,” according to the Washington State Nurses Association. The technical reality—including the need for human support to move Moxi between floors—meant the robots “would never deliver meaningful time savings.”

By January 2026, Diligent was acquired by Serve Robotics, a sidewalk delivery company based in Redwood City, California—a strategic exit suggesting the hospital robotics path faced challenges that raw deployment numbers didn’t capture.

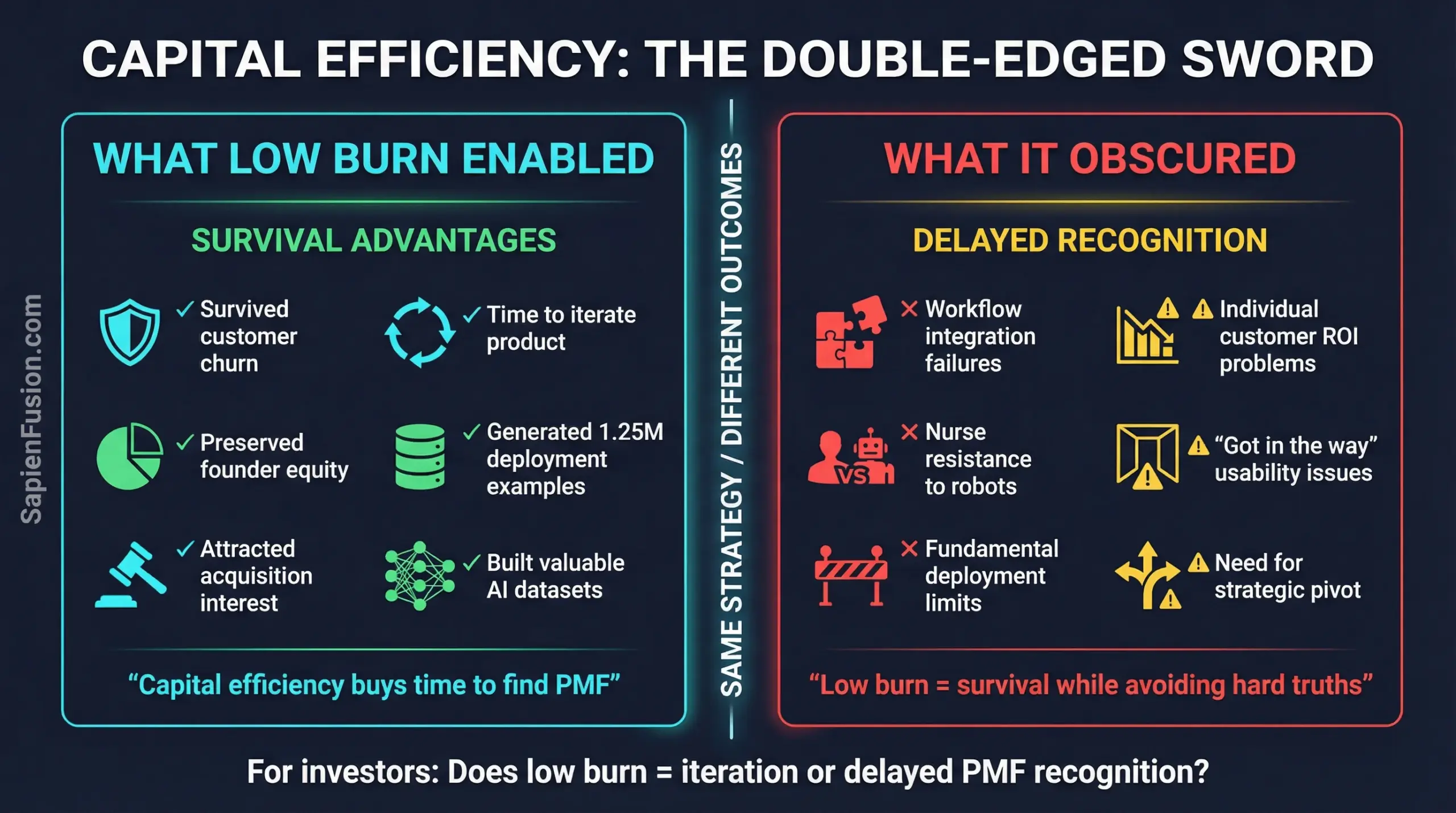

This is the paradox of capital-efficient deployment: low burn rate enables survival through customer churn that would bankrupt higher-cost competitors. The question isn’t whether Thomaz built impressive technology with limited capital—she demonstrably did. The question is whether capital efficiency can mask product-market fit problems until they become strategic exits.

The Twenty-Year Thread

When Thomaz joined a robotics lab at MIT in 2002, she became “obsessed with the same high-level technical goal” she’s pursuing today: making it so people can “just demonstrate something to a robot and the robot then knows what to do.”

Her 2006 PhD dissertation, “Socially Guided Machine Learning” under Cynthia Breazeal, established the foundational approach. Traditional machine learning required programmers. Thomaz wanted robots that learned from human teachers the way children learn—through demonstration, feedback, and social cues.

For nine years (2007-2016), she built that vision at Georgia Tech, directing the Socially Intelligent Machines Lab and advising PhD students including Vivian Chu, who would become her co-founder. Her robots—Simon, learning to sort blocks; others learning household tasks—demonstrated the technical viability. What they lacked was a market that needed them badly enough to pay for imperfect automation.

“I was almost embarrassed to say that I’ve been obsessed with this problem for 20 years,” Thomaz reflected in 2022. “But look how far we’ve come!”

That persistence through constraint—maintaining focus on one hard technical problem while the field evolved around her—would prove essential when Diligent needed to deploy robots in chaotic hospital environments where failure wasn’t academic.

The NSF Commercialization Path

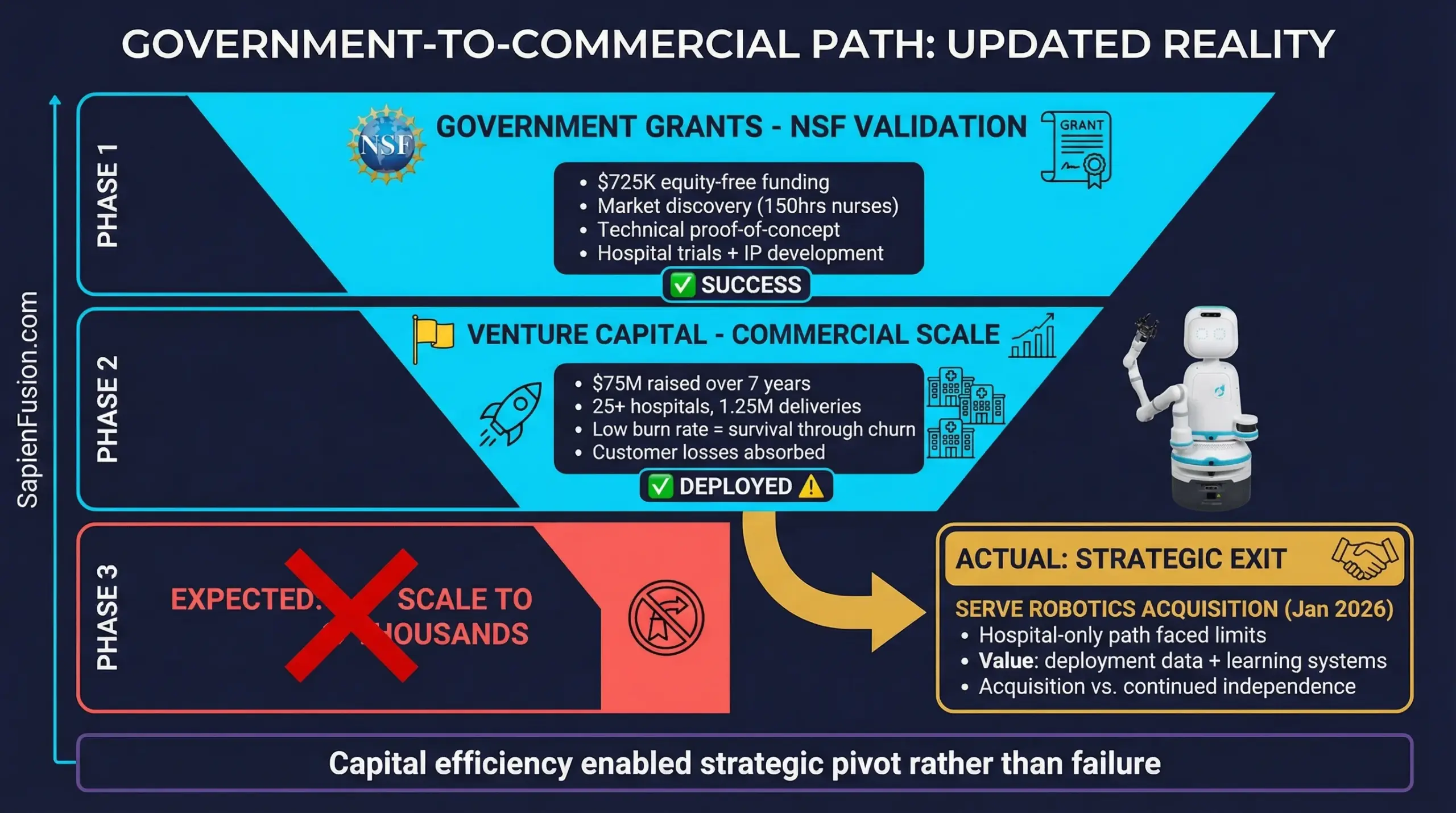

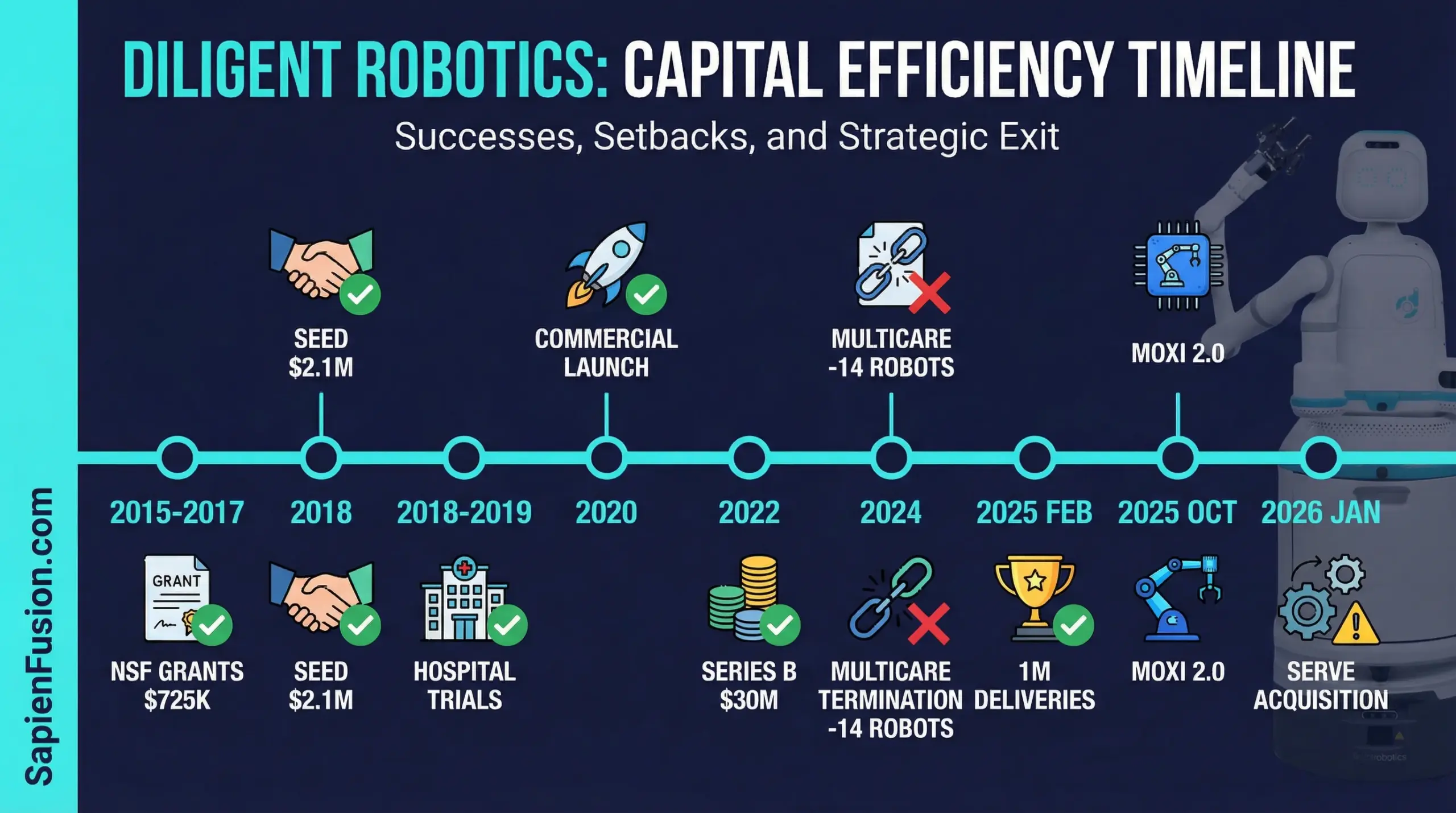

In 2015, Thomaz and Chu didn’t start with a pitch deck and a Series A target. They started with a six-month $225,000 NSF I-Corps grant to “think about the market that would be good for robots.”

Most robotics companies skip this step. They build impressive technology, then search for customers. Thomaz inverted the sequence: 150 hours following nurses and nursing assistants across three Austin hospitals, documenting why healthcare professionals were “hunting and gathering” for supplies when they should be providing patient care.

The structural demand was acute. Hospitals were already “pretty high-tech” with “sophisticated staff in terms of usage of technologies,” making them ideal environments for automation. More critically, the nursing shortage wasn’t speculative—it was an operational crisis affecting every hospital system.

That market validation led to an NSF SBIR Phase II grant for $500,000 in 2017. With that $725,000 in equity-free government funding, Diligent partnered with four Texas health systems to complete research trials. “We built some of the core technology around the interactive machine learning that allows our robots to quickly be deployed to new settings,” Thomaz explained. “That led to some of our first patents and was really kind of the foundation of the company.”

Only after proving technical viability in real hospitals did Diligent raise a $2.1 million seed round led by True Ventures in January 2018.

This is capital-efficient de-risking: government grants fund market discovery and technical proof-of-concept, preserving equity and demonstrating commercial traction before institutional capital arrives.

The Social Intelligence Thesis

Moxi doesn’t try to be autonomous. It’s designed around a fundamental insight from Thomaz’s two decades of research: robots working alongside people in unstructured environments need social intelligence more than full autonomy.

The robot navigates hospital hallways, opens elevators and doors independently, avoids colliding with people or equipment, and “happily poses for selfies” when staff want photos. It uses facial and voice recognition to verify deliveries to the right person. When it encounters ambiguous situations, it asks humans for help rather than making incorrect assumptions.

This isn’t the humanoid robotics playbook. Moxi has arms and grippers for mobile manipulation, but its core technical advantage is human-guided learning. “The more your staff uses Moxi, the more Moxi learns and adapts to your environment and way of doing things,” Diligent’s technical documentation states.

Every interaction generates training data. More deployments improve the visual language models that enable “semantic scene understanding in a busy human, indoor environment”—different from autonomous cars or drones operating in outdoor spaces with clearer sensor data.

By March 2025, one million deliveries meant the robots were “continually learning about being mobile and manipulating” in exactly the environments where they needed to operate. That compounding data advantage doesn’t require betting on autonomous breakthrough—it builds competitive moat through operational deployment.

The Pandemic Acceleration

Between 2018 and early 2020, Diligent was methodically scaling. “A couple of years ago, if we were working with a hospital it was because they had some special funds set aside for innovation or they had a CTO or a CIO that had a background in robotics,” Thomaz noted in 2022. “But it certainly wasn’t the first thing that every hospital CIO was thinking about.”

Then came COVID-19.

“Now that has completely changed,” Thomaz continued. “We’re getting cold outreach on our website from CIOs of hospitals saying ‘I need to develop a robotic strategy for our hospital and I want to learn about your solution.’ Through the pandemic, I think everyone has seen that the workforce shortage in hospitals is only getting worse.”

Mary Washington Healthcare’s experience exemplified the shift: “We started implementing Moxi into our clinical workflows in December and planned on going through a trial phase to determine if the technology would be helpful to our staff. Right away, we could see the impact Moxi made on the efficiency of our staff and how morale immediately increased. We were so impressed with what Moxi took off our team’s hands, we chose to add even more robots to our fleet.”

In April 2022, Diligent raised $30 million in Series B funding led by Tiger Global, bringing total capital raised to ~$50 million. By September 2023, they added $25 million more.

That’s ~$75 million total raised over seven years to achieve 1 million deliveries across dozens of hospitals. By comparison, Jibo raised $73 million, shipped thousands of robots to consumers, then shut down when the novelty wore off.

The Deployment Metrics

Moxi’s core workflows span the mundane tasks that consume healthcare professionals’ time without requiring their expertise:

Laboratory deliveries: Transporting lab samples between floors and departments, eliminating nurse trips to central labs.

Medication transport: Moving pharmacy deliveries to patient floors, enabling “Meds to Beds” programs where patients receive prescriptions before discharge.

Supply replenishment: Delivering wound dressings, IV supplies, and equipment between storage and clinical areas.

Personal item transfers: Moving patient belongings or lightweight equipment between units.

When Moxi completed its millionth delivery in March 2025, it was delivering medication to an outpatient infusion center in Chicago—a workflow where speed directly impacts patient experience. Cancer patients arriving for chemotherapy treatments need their medications immediately to minimize time in the clinic.

“The pharmacy is far from the infusion center,” Thomaz explained. “We hear a lot from the infusion clinic teams that use Moxi that they just love seeing the efficiency. They love seeing that people can get in the chair and get their meds started right away.”

Each deployment follows a 12-week implementation timeline: Diligent’s team customizes operational workflows for the specific hospital environment, trains staff on interacting with Moxi, and integrates the robot into existing clinical systems.

The business model is Robotics-as-a-Service (RaaS). “Cost is based on the customized utilization of each Moxi robot for every hospital’s particular needs,” Thomaz noted. This recurring revenue model aligns incentives—Diligent succeeds when hospitals see sustained value, not one-time hardware sales.

Strategic Positioning: Healthcare First, Then Adjacent Markets

Diligent isn’t trying to build “the robot for everything.” They’re building trust and technical capability in one demanding vertical, then expanding.

“If we go from hospitals to assisted living, for example, then you start to see a very interesting trajectory where a company could go from hospitals to structured nursing homes to eventually the home,” Thomaz outlined in 2025. “I personally think there are a lot of companies going out and going straight to humanoids for the home. But we’ve kind of taken this very concerted path to become a trusted partner in healthcare.”

The technical progression makes strategic sense. Hospitals are semi-structured environments with clear workflows, sophisticated users comfortable with technology, and acute pain points that justify automation costs. Success there builds credibility for less-structured environments.

Current expansion focuses on patient-facing tasks: delivering pillows, water, or comfort items directly to patient rooms. These workflows would translate directly to assisted living facilities, where similar delivery tasks exist but with residents rather than patients.

The market opportunity is substantial. The global smart hospital market was estimated at $27.6 billion in 2021, projected to reach $82.89 billion by 2026, compounding at 24.6% annually. Robotic automation addresses the core constraint: workforce shortages that limit hospital operational capacity regardless of available beds or equipment.

The Academic-to-Commercial Bridge

Thomaz’s path illustrates a capital-efficient model for translating frontier research into commercial deployment:

Phase 1 (2002-2015): Academic Foundation Build deep technical expertise in a focused problem domain. Thomaz’s MIT dissertation and Georgia Tech lab established her as a leading authority on socially-guided machine learning and human-robot interaction. This expertise became competitive moat when deploying in complex environments.

Phase 2 (2015-2017): Government-Funded Market Discovery NSF grants funded rigorous customer discovery (150 hours shadowing nurses) and technical proof-of-concept in real environments. This de-risked both market and technical assumptions before raising venture capital.

Phase 3 (2017-2020): Controlled Commercial Deployment Seed funding enabled partnerships with four Texas health systems for research trials. Learning from these deployments shaped product design, operational workflows, and business model before scaling.

Phase 4 (2020-present): Scale Against Proven Demand Pandemic-driven urgency validated the thesis. Series B and subsequent funding accelerated deployment to dozens of hospitals, with each installation improving the underlying machine learning models.

This contrasts sharply with venture-first approaches where companies raise large rounds, build impressive demos, then search for customers willing to pay. Thomaz spent years validating demand and refining technology in real environments before seeking institutional capital.

The Recognition Pattern

MIT Technology Review’s 35 Under 30 | Popular Science’s Brilliant 10 | National Academy of Science Kavli Fellow | Presidential Council of Advisors on Science and Technology | Texas Monthly’s Most Powerful Texans 2018

These aren’t vanity metrics—they’re validation that Thomaz’s approach to socially intelligent robotics represents genuine technical innovation with commercial viability. The recognition came from both academic institutions (National Academy) and industry publications (MIT Tech Review), signaling cross-domain impact.

More tellingly, her co-founder Vivian Chu received MIT Technology Review’s 35 Under 35 in 2019, and Thomaz was named to Inc. Magazine’s 100 Female Founders Building America’s Most Innovative Businesses. These awards recognize execution, not just research potential.

The MultiCare Termination: When Deployment Metrics Diverge From Customer Value

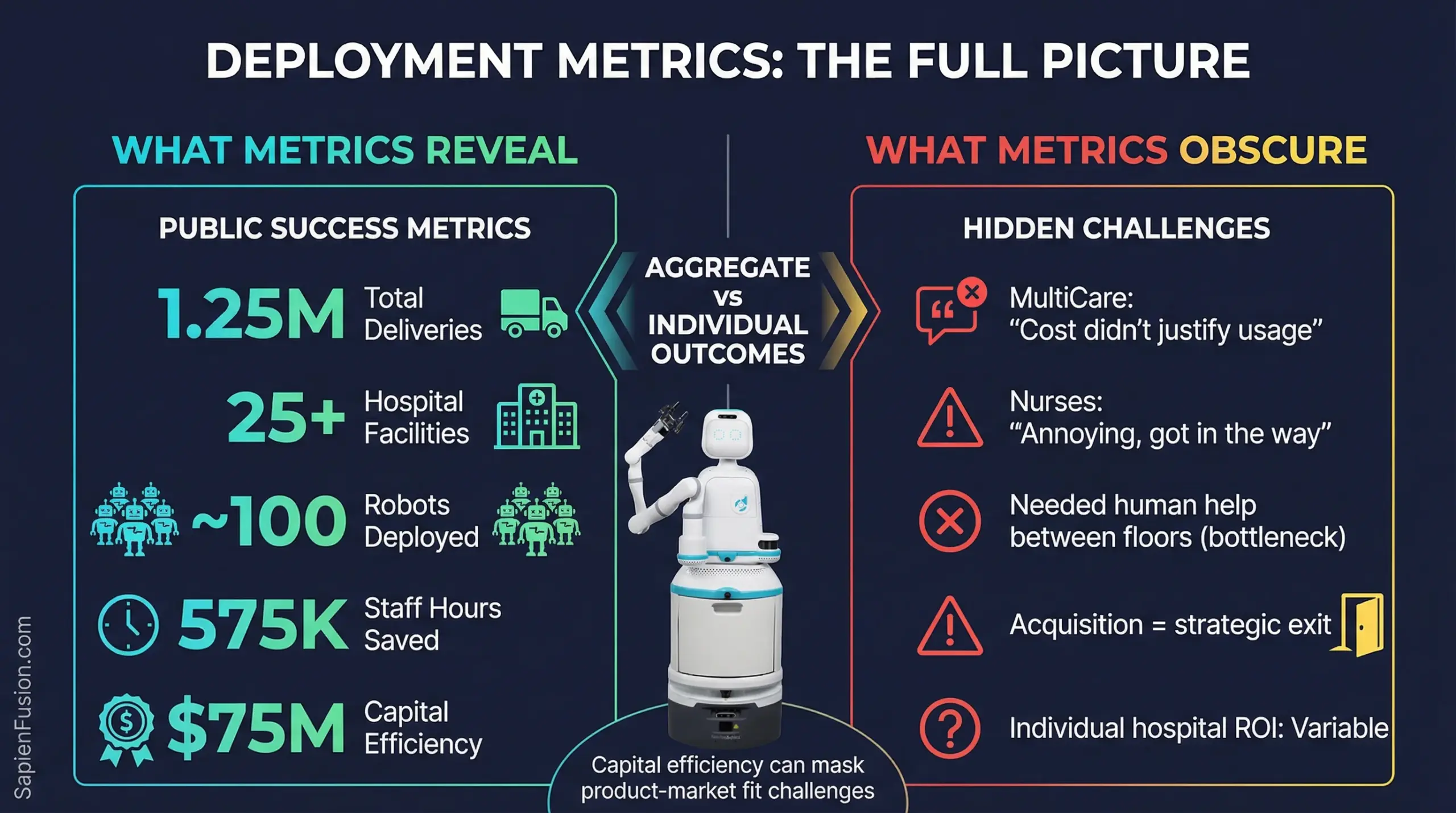

While Diligent publicly celebrated deployment milestones, not all customers saw sustained value. In February 2024—approximately one year before the company announced its millionth delivery—MultiCare Health System in Tacoma, Washington terminated its contract after deploying 14 Moxi robots across facilities in Puget Sound and Eastern Washington.

MultiCare’s explanation was blunt: “We found it wasn’t financially sustainable for us to keep using the robots. The cost didn’t justify their level of usage.”

The Washington State Nurses Association, representing nurses at Tacoma General Hospital and Good Samaritan Hospital, reported that “the Moxi robots were annoying and often got in the way.” More fundamentally, “the technical realities, including the need for human support to move Moxi between floors, meant it would never deliver meaningful time savings.”

This represents a critical tension in capital-efficient deployment strategies: low burn rates enable companies to survive customer churn that would bankrupt higher-cost competitors. Diligent’s ~$75 million raised over seven years meant losing MultiCare’s 14-robot deployment didn’t force immediate strategic changes. A competitor that raised $200 million and burned proportionally faster might not have survived comparable customer losses.

The acquisition by Serve Robotics in January 2026 suggests this wasn’t an isolated challenge. Serve, which operates sidewalk delivery robots for food and goods, saw Diligent’s hospital deployment experience as valuable—but the deal structure (acquisition rather than partnership or continued independent growth) indicates the hospital-only path faced limitations.

“Indoor environments, such as hospitals, add a powerful new dimension to Serve’s Physical AI flywheel,” the acquisition announcement stated. The emphasis on “flywheel” and shared autonomy stacks suggests Serve valued Diligent’s deployment data and learning systems more than its hospital customer base.

The Moxi 2.0 Pivot: Betting on Technology When Customer Traction Wavers

In October 2025—months after the MultiCare termination but before the Serve acquisition—Diligent unveiled Moxi 2.0 at NVIDIA’s AI conference. Built on NVIDIA IGX Thor (Blackwell-powered) with 10x the compute of Moxi 1.0, the new platform represented a significant technical advancement.

The timing is revealing. When customer traction weakens, capital-efficient companies often double down on technology improvements, hoping better products will solve adoption problems. Moxi 2.0’s robot foundation model, enhanced manipulation capabilities, and predictive inference could genuinely address limitations that frustrated MultiCare’s nurses.

But technology improvements don’t solve fundamental workflow integration challenges. If nurses need to assist robots between floors, if robots “get in the way” in busy corridors, if the ROI doesn’t justify operational costs—these aren’t compute power problems. They’re deployment model problems.

Diligent hired two former Cruise executives (Rashed Haq as CTO, Todd Brugger as COO) in summer 2025, suggesting recognition that autonomous vehicle deployment experience might transfer to hospital robotics. The subsequent Serve acquisition—merging with a company specializing in outdoor sidewalk delivery—indicates the hospital-focused strategy had reached inflection points requiring strategic alternatives.

Strategic Implications: The Capital Efficiency Double Edge

Diligent’s trajectory reveals both the power and limitations of capital-efficient deployment:

What Worked:

1. Government grants for systematic de-risking $725K in NSF funding enabled market discovery (150 hours shadowing nurses) and technical validation in real hospitals before venture capital. This preserved equity and demonstrated commercial viability, reducing investor risk when institutional funding arrived.

2. Deploy early, learn in real environments Hospital trials (2018-2019) shaped product design, operational workflows, and business model before commercial launch. Each deployment generated training data that improved visual language models and manipulation capabilities.

3. Social intelligence over autonomous completeness Robots that work alongside people don’t need to solve every edge case autonomously. Human-guided learning creates training data while accomplishing useful work—in theory.

4. Twenty-year technical focus positioned for market timing Thomaz’s persistence on human-guided machine learning meant the technology was ready when pandemic-driven workforce shortages made hospital automation urgent rather than experimental.

What the Metrics Obscured:

1. Deployment count ≠ customer retention 1.25 million deliveries across 25+ hospitals sounds impressive until you learn MultiCare (14 robots) terminated citing cost/value mismatch. Aggregate metrics can mask individual customer failures.

2. Low burn rate enables survival through churn ~$75 million over seven years meant Diligent could lose major customers without immediate existential crisis. Higher-cost competitors would face investor pressure after comparable losses. This is capital efficiency—but it can delay addressing fundamental product-market fit issues.

3. Technical improvements don’t solve workflow problems Moxi 2.0’s 10x compute increase addresses AI capabilities, not the operational realities nurses cited: needing human help between floors, robots blocking corridors, ROI not justifying costs. These are deployment model challenges, not technology challenges.

4. Acquisition as strategic exit Being acquired by a sidewalk delivery robot company (completely different domain) suggests the hospital-only path faced growth limitations. Serve valued Diligent’s deployment data and learning systems more than its customer base.

The Broader Lesson:

Capital efficiency in frontier robotics enables time to find product-market fit without burning through runway. For Diligent, that meant surviving long enough to accumulate 1.25 million delivery examples and develop robot foundation models that attracted Serve’s acquisition interest.

But capital efficiency doesn’t guarantee customer value. When MultiCare’s nurses reported robots “got in the way” and “would never deliver meaningful time savings,” more compute power or better AI models wouldn’t solve the fundamental workflow integration challenge.

The question for operators: Does your capital efficiency buy time to iterate toward genuine product-market fit, or does it enable survival while avoiding hard truths about customer value?

The question for investors: Do deployment metrics represent validated customer demand or capital-efficient persistence through churn?

Thomaz built impressive technology with limited capital, deployed in complex real-world environments, and generated valuable datasets. The Serve acquisition suggests that value was real—just not necessarily in the form of a standalone hospital robotics company scaling to thousands of deployments by 2030.

Learn More About Andrea Thomaz and Diligent Robotics

Company & Product:

- Diligent Robotics Official Website

- Andrea Thomaz Profile

- Series B Funding Announcement (April 2022)

- 1 Million Deliveries Milestone (March 2025)

Academic Background:

- Andrea Thomaz Google Scholar

- Socially Intelligent Machines Lab Publications

- MIT Media Lab Alumni Profile

Government Commercialization Path:

Interviews & Insights:

- Ubiquity Ventures Founder Profile (2022)

- Robohub Interview on Series B and Demand (2022)

- American Healthcare Leader Profile

Recognition:

- MIT Technology Review 35 Under 35

- Popular Science Brilliant 10

- National Academy of Science Kavli Fellow

- Texas Monthly Most Powerful Texans 2018

- Inc. Magazine 100 Female Founders 2019

This is Part 6 of 7 from The Capital Efficiency Paradox

All parts in this series:

- Part 1: Capital Efficiency Through Humanoid Telepresence

- Part 2: Building the First Longitudinal Women’s Health Dataset

- Part 3: $800M to Rebuild Drug Discovery

- Part 4: $230M to $1B in Four Months

- Part 5: From 20 Researchers to 2.7 Billion Downloads

- Part 6: Capital Efficiency Through Government-to-Commercial Path

- Part 7: The Capital Efficiency Playbook

- Research Methodology and Source Verification for the Capitol Efficiency Paradox Series